In the world of SEO, we are obsessed with “efficiency.” We want the fastest site speeds, the most authoritative backlinks, and the highest ROI. When it comes to your personal finances, the ultimate efficiency play is figuring out can you pay your mortgage with a credit card.

As of April 18, 2026, the landscape has changed significantly. We’ve moved beyond the “gray hat” tactics of the past and into a new era of fintech where even your biggest monthly expense can fuel your next vacation. However, just like a complex SEO audit, you need to understand the technical “backend” of these transactions. Mortgage lenders generally do not accept credit card payments directly because of the 3% merchant fees. But with the right middleware and the latest 2026 card products, you can bridge that gap.

1. The Bilt Card 2.0 Revolution: No-Fee Rewards

The most significant update to the question can you pay your mortgage with a credit card came in January 2026 with the launch of the Bilt Card 2.0.

Unlike traditional cards, Bilt provides a specialized routing and account number that acts as a “proxy” for your credit line. You can use these details in your mortgage lender’s online portal just like a standard bank account. Bilt then charges your credit card for the amount.

The 2026 Advantage:

- Zero Transaction Fees: Bilt allows you to pay your mortgage with no transaction fee.

- Tiered Earning: You can earn up to 1.25X Bilt Points on housing payments based on your monthly spending.

- Flexible Earning: You can choose between “Housing-only” rewards or a mix of points and “Bilt Cash.”

This is the “Featured Snippet” of mortgage payments—it bypasses the standard rules and provides direct value without the cost.

2. Third-Party Services: The Plastiq “Redirect”

If you don’t have a specialized housing card, you might wonder can you pay your mortgage with a credit card using a third-party service. Plastiq remains the industry standard for this “redirect” maneuver.

How it works:

- You charge your credit card through Plastiq’s platform.

- Plastiq charges you a 2.99% base fee.

- Plastiq sends a paper check or ACH transfer to your mortgage servicer on your behalf.

While a 2.99% fee sounds like a “negative ranking signal” for your wallet, it can be mathematically sound if you are working toward a large Sign-Up Bonus (SUB). If spending $4,000 earns you 80,000 miles (valued at $1,200), the $120 fee is a small price to pay for the “conversion.”

3. The Mastercard and Discover Advantage

One technical detail often missed in the can you pay your mortgage with a credit card discussion is the card network policy. As of 2026, Visa and American Express still maintain strict “anti-churning” policies that prevent their cards from being used for mortgage payments through third-party services like Plastiq.

If you want this strategy to “index” correctly, you must use a Mastercard or Discover card. These networks are much more permissive regarding “debt-for-debt” payments, provided the transaction is coded correctly as a utility or professional service payment.

4. Comparing the ROI: Fees vs. Rewards (Table)

When deciding can you pay your mortgage with a credit card, you must run a “competitor analysis” on your rewards vs. the fees.

2026 Cost-Benefit Analysis

| Payment Method | Transaction Fee | Rewards Earned (on $3,000) | Net Result |

|---|---|---|---|

| Bilt Card 2.0 | 0% | 3,000 – 3,750 Points | Win (+Value) |

| Plastiq (2% Card) | 2.99% ($89.70) | $60.00 | Loss (-$29.70) |

| Plastiq (Sign-Up Bonus) | 2.99% ($89.70) | $500.00+ Value | Win (+Value) |

| Direct Lender Pay | N/A (Rare) | N/A | N/A |

Export to Sheets

5. Using Balance Transfer Checks as a Buffer

Another manual workaround for can you pay your mortgage with a credit card is using “convenience checks” or balance transfer offers. Many credit cards in 2026 still offer 0% APR for 12–15 months on balance transfers.

You can write one of these checks directly to your mortgage servicer. This effectively moves your mortgage debt to your credit card at 0% interest for a year. The “entry price” is usually a 3% to 5% upfront fee. This is only recommended if you are in a temporary cash-flow crunch and want to avoid the 6.34% interest accruing on your mortgage for a few months.

6. The “Black Hat” Risks: Credit Utilization

Just because you can doesn’t mean you should without a strategy. In SEO, if you build too many backlinks too fast, you get penalized. In credit, if you put a $4,000 mortgage on a $10,000 limit card, your Credit Utilization spikes to 40%.

This is a “negative ranking signal” to FICO. Even if you pay the card off a week later, if the balance is reported to the bureau while it’s high, your credit score could drop by 20 to 50 points. If you are asking can you pay your mortgage with a credit card, always ensure you have a high enough credit limit to keep your utilization below 30%.

7. Business Credit Cards and Melio

For the entrepreneurs and bloggers out there, Melio is a powerful tool. While primarily a B2B platform, some use it to pay property-related expenses. Using a Business Credit Card for can you pay your mortgage with a credit card queries is often safer because business debt usually doesn’t report to your personal credit profile, keeping your personal “Financial Authority” high.

8. Avoiding the “Cash Advance” Trap

Never, under any circumstances, should you use your credit card to take out a cash advance to pay your mortgage.

- No Grace Period: Interest starts accruing the second the cash hits your hand.

- High APR: Usually 29.99% or higher.

- Extra Fees: Often a flat 5% fee upfront.

When you research can you pay your mortgage with a credit card, ensure the method you choose is coded as a “purchase” or “payment service,” not a “cash equivalent.”

9. Timing Your “Crawl”: Transaction Latency

One critical factor in can you pay your mortgage with a credit card is the processing time. A service like Plastiq has to mail a physical check in many cases.

- ACH Transfer: 3–5 business days.

- Paper Check: 7–10 business days.

If your mortgage is due on the 1st and you initiate the payment on the 30th, you will likely be hit with a late fee. In SEO, we call this “latency.” Always initiate your credit card mortgage payments at least 14 days before the grace period ends.

10. The 2026 Market Context

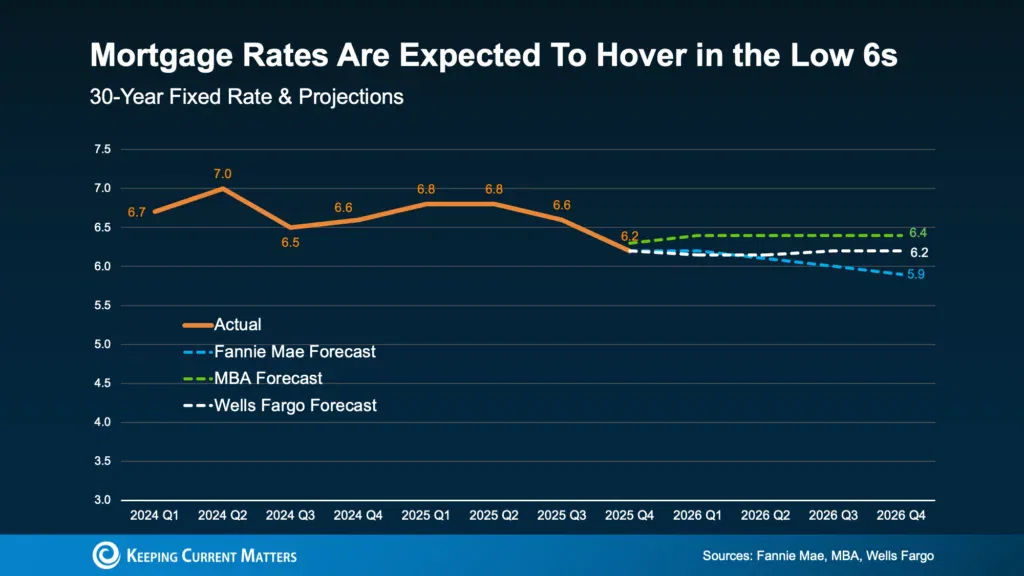

With 2026 interest rates currently averaging 6.34%, carrying a balance on a credit card (at 24%) is a financial disaster. Only ask can you pay your mortgage with a credit card if you have the cash sitting in a high-yield savings account ready to pay off the statement.

The goal here is “Arbitrage”—you want to earn the 4.5% interest in your savings account and the credit card points, while paying off the card before a single penny of 24% interest is charged.

Frequently Asked Questions (FAQs)

Can you pay your mortgage with a credit card directly?

No. Most mortgage lenders do not accept credit cards directly because they do not want to pay the 3% processing fees. You must use a third-party service or a specialized card like Bilt.

Is there a fee for paying mortgage with a credit card?

If you use a service like Plastiq, the fee is typically 2.99%. If you use the Bilt Card 2.0, there is no transaction fee.

Does paying my mortgage with a credit card help my credit score?

If you keep your utilization low and pay the card in full every month, it can help by showing a history of large, on-time payments. However, a high balance on your statement date can cause your score to drop temporarily.

Can I use an American Express card to pay my mortgage?

Generally, no. As of 2026, Amex and Visa have blocked most mortgage payments through third-party services. You are usually required to use a Mastercard or Discover.

What is the “Bilt Cash” mentioned in 2026 reviews?

Bilt Cash is a new rewards currency for 2026 that gives you 4% back on everyday spend, which can then be used to “unlock” or boost the points you earn on your mortgage payments.

Is it worth it for the miles and points?

It is only worth it if the value of the rewards is higher than the transaction fee. For most 1% or 2% cashback cards, the 2.99% fee makes it a losing deal unless you are hitting a sign-up bonus.

Conclusion

The answer to can you pay your mortgage with a credit card is a nuanced “Yes, but you need a technical strategy.” In 2026, the arrival of Bilt Card 2.0 has made this more accessible than ever, essentially allowing you to earn rewards on your largest expense for free.

By treating your mortgage like a high-authority project, you can optimize your “conversion” rate for travel points and cash back. Just remember the SEO golden rules: avoid “black hat” cash advances, monitor your “technical debt” (interest), and always ensure your utilization stays in the “green zone.”

Now that you know the backend of can you pay your mortgage with a credit card, it’s time to audit your wallet. Pick the right card, calculate your break-even point, and start turning your mortgage into your next first-class flight.

Disclaimer: This guide is for informational purposes only. Using credit cards for large debt payments involves financial risk. Consult a financial advisor to see how this strategy fits into your overall budget.